Taxpayers Forced To Insure A Foster Care System That Cannot Insure Itself

Alecomm is disgusted that physical and sexual abuse within out-of-home care has become such a recognised financial risk that governments are now creating taxpayer-funded indemnity schemes to protect the organisations responsible for caring for vulnerable children.

Let that sink in.

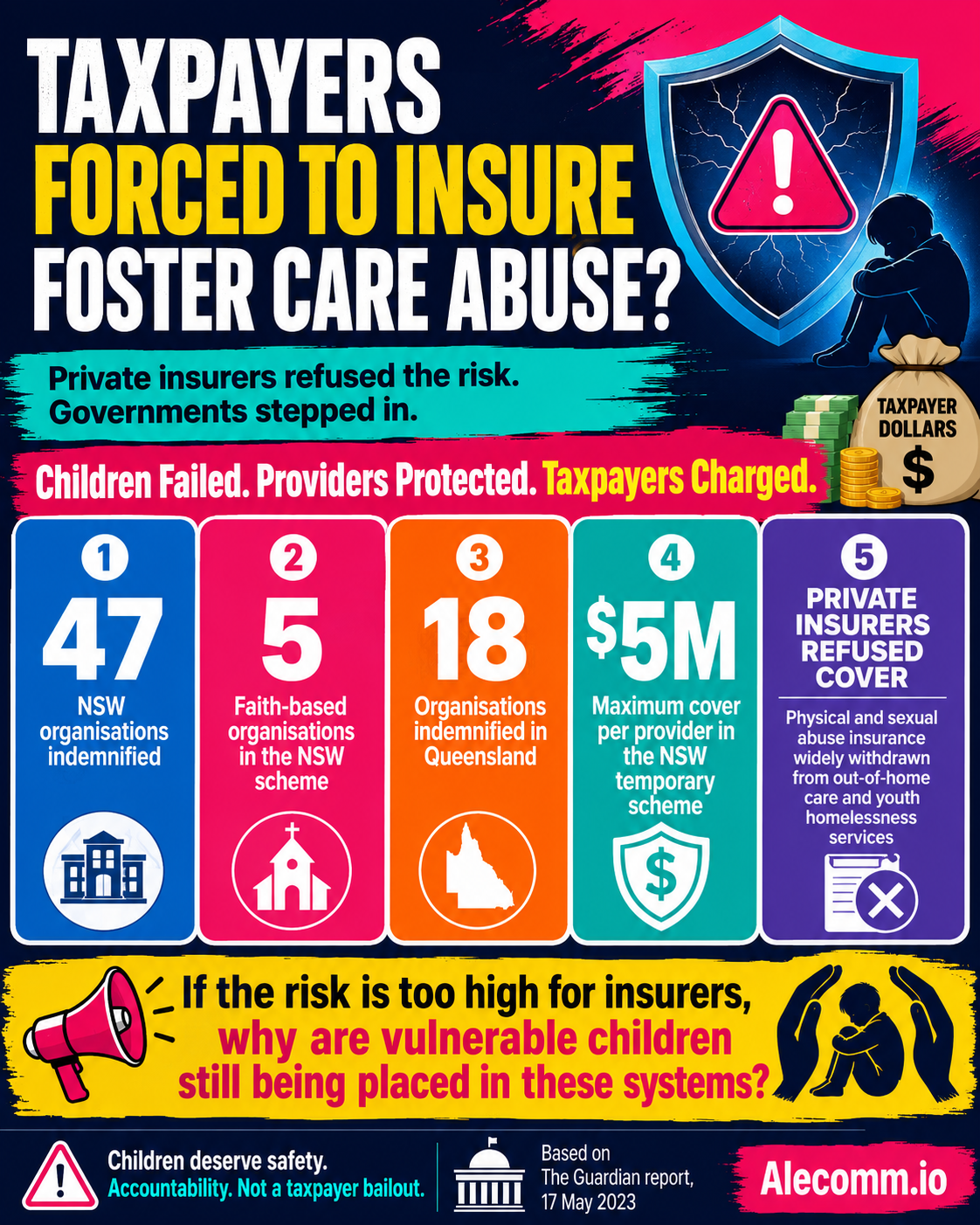

Private insurers have examined the risk associated with organisations operating foster care, residential care and youth homelessness services and, in many cases, have refused to provide physical and sexual abuse coverage.

The risk is apparently considered too serious, too unpredictable or too expensive for commercial insurers.

So who has been forced to carry that risk instead?

The Australian taxpayer.

According to reporting published in May 2023, the New South Wales Government entered indemnity arrangements with 47 non-government organisations providing out-of-home care and youth homelessness services.

Five of those organisations were faith-based.

Queensland reportedly indemnified another 18 organisations, including Anglicare Southern Queensland and four other church or faith-based providers. Western Australia and Tasmania also confirmed that they were providing indemnity arrangements to affected organisations.

This is not simply an insurance problem.

It is an accountability problem.

The Public Is Being Forced To Carry The Risk

Governments argue that these organisations provide essential services and may be forced to stop operating without insurance.

- But this creates an extraordinary and morally repugnant arrangement.

- The organisations receive government funding to care for vulnerable children.

- When children are harmed, the organisations may face legal claims.

- Private insurers refuse to cover the risk.

- The government then steps in and uses public money to indemnify the providers.

In other words, taxpayers fund the placement, taxpayers fund the organisation, taxpayers fund the government departments overseeing the placement, and taxpayers may then be forced to fund compensation when the placement results in physical or sexual abuse.

Meanwhile, the organisations responsible can continue operating.

- Where is the personal responsibility?

- Where is the corporate responsibility?

- Where is the government accountability?

And most importantly:

Where is the protection for the child?

This Is More Than A “Market Failure”

Government representatives have described the withdrawal of private insurance as a form of “market failure”.

Alecomm rejects that sanitised description.

- The insurance market has not simply suffered an unexplained technical malfunction.

- Insurers make decisions based on risk.

- When insurers refuse to cover a particular category of harm, it indicates that they believe the likelihood or financial consequences of claims are too great to accept under ordinary commercial conditions.

The real question is not merely why insurers have withdrawn.

The real question is:

Why has the risk of physical and sexual abuse within services for vulnerable children become so serious that private insurers do not want to touch it?

Calling this a market failure shifts attention away from the child protection system, the organisations delivering the services, the departments responsible for oversight and the governments responsible for contracting them.

This is not a discussion about damaged buildings, stolen vehicles or workplace accidents.

- It is insurance specifically designed to respond to allegations and claims involving the physical and sexual abuse of children and vulnerable young people.

- The fact that an entire inter-jurisdictional government working group was established to find a long-term insurance solution should horrify every Australian.

- Governments appear to be working urgently to solve the insurance problem.

Alecomm wants to know why they have not shown the same urgency in solving the abuse problem.

Removing Limitation Periods Exposed The True Liability

The withdrawal of insurance followed legal reforms removing time limits on civil child abuse claims. Those reforms allowed survivors to bring claims that had previously been blocked simply because too much time had passed.

- This was necessary because many survivors of childhood abuse cannot disclose what happened to them until years or even decades later.

- The resulting increase in claims did not create the underlying abuse.

- It exposed the liability that had already been buried.

- Once survivors were given a greater opportunity to seek justice, the true financial risk to institutions became harder to conceal.

Private insurers responded by withdrawing coverage. And then – Governments responded by creating indemnity schemes.

But the public should be asking whether these arrangements protect survivors and children, or whether they primarily protect organisations from the financial consequences of institutional failure.

The NSW Scheme

The New South Wales temporary indemnity scheme reportedly covered 47 providers of out-of-home care and youth homelessness services.

The scheme was available where an organisation had been unable to obtain physical and sexual abuse insurance through the commercial market.

Each provider was covered for up to $5 million, including associated costs such as legal defence costs.

- The scheme only applied to abuse occurring after 30 June 2017.

- Any costs above the $5 million limit were to be borne by the provider.

- Providers were also required to pay a fee to participate.

- These limitations do not alter the central issue.

The government accepted that taxpayer-backed financial protection was necessary to keep these organisations operating.

That decision may preserve service delivery, but it also risks protecting a fundamentally broken contracting model.

If an organisation cannot obtain insurance because the risk of abuse claims is considered commercially unacceptable, the automatic response should not be to transfer that risk to the taxpayer.

The first response should be an independent investigation into the organisation’s governance, complaint history, staffing practices, placement decisions, incident reporting, internal culture and record of protecting children.

Church-Linked Organisations Must Not Be Shielded

The involvement of church and faith-based organisations makes this issue even more disturbing.

Many religious institutions already possess significant assets, property holdings, charitable structures and established legal resources.

Taxpayers should not be forced to provide financial protection to powerful institutions while survivors are left fighting for recognition, records, compensation and justice.

A religious or charitable identity must never be treated as a substitute for accountability.

Nor should the threat of service disruption be used to frighten governments into insulating providers from the consequences of abuse.

Where an organisation cannot safely provide care, the answer is not to shield it indefinitely.

The answer is to replace it.

The System Protects Service Continuity Before Children

The official justification for these indemnity schemes is that governments rely on non-government organisations to deliver critical out-of-home care and youth homelessness services.

That statement reveals the deeper structural problem.

Governments have outsourced so much responsibility that they now fear the collapse of private and charitable providers more than they fear the continuation of institutional harm.

Instead of maintaining sufficient public capacity to care for children directly, governments have created dependency on contracted organisations.

Those organisations can then become effectively too important to fail.

- When private insurers withdraw, governments feel compelled to intervene because they no longer have the capacity to replace the providers.

- This leaves taxpayers underwriting a system they do not control, while children are placed inside services that governments claim they cannot afford to lose.

- That is not genuine child protection.

It is institutional self-preservation.

What Alecomm Demands

Alecomm believes no organisation should receive taxpayer-funded indemnity for physical or sexual abuse claims without intensive, independent and continuing scrutiny.

Every participating organisation should be required to publicly disclose:

- The number of abuse allegations received.

- The number of allegations reported to police.

- The number of children removed from placements following complaints.

- The number of staff, carers or contractors suspended or dismissed.

- The value of claims, settlements and legal defence costs.

- Any prior findings of misconduct, systemic failure or inadequate supervision.

- The organisation’s assets, reserves and capacity to contribute to compensation.

- The names of related entities receiving government funding.

Government departments should also be required to disclose what warnings they received, what action they took, whether contracts were renewed after serious incidents and whether children remained in placements after allegations were made.

- Indemnity must never become immunity.

- Taxpayer protection must be built into every arrangement.

Organisations found to have concealed abuse, ignored complaints, retaliated against whistleblowers, destroyed records or failed to report criminal conduct should lose access to indemnity and government contracts.

Senior executives and directors should also face consequences where serious governance failures are established.

Children Are Not An Insurable Operational Risk

The language used around this issue is cold and bureaucratic.

- “Physical and sexual abuse insurance.”

- “Indemnity arrangements.”

- “Market failure.”

- “Service continuity.”

- “Long-term solutions.”

Behind those phrases are children who may have been assaulted, exploited, ignored or silenced while living in systems that were supposed to protect them.

Abuse must never be treated as an unavoidable operational risk of foster care.

It is not equivalent to property damage or public liability.

It is the catastrophic failure of the very purpose for which these organisations are funded.

Alecomm is disgusted that governments appear prepared to accept abuse liability as a predictable cost of outsourcing child protection.

We are equally disgusted that taxpayers are being forced to carry the financial consequences while the same institutions continue receiving contracts and public funding.

The public deserves to know why these organisations cannot obtain insurance.

Survivors deserve compensation without being forced through years of litigation.

Children currently in care deserve far more than another insurance scheme designed after the damage has already occurred.

They deserve a system that prevents the abuse in the first place.

Until governments prioritise prevention, transparency and accountability over protecting providers, these indemnity schemes will remain what they truly are:

Taxpayer-funded protection for a child protection system that has repeatedly failed to protect children.

Source

- Knaus, C. (2023, May 17). NSW taxpayers to fund indemnity for 47 organisations against child abuse claims. The Guardian. https://www.theguardian.com/australia-news/2023/may/17/nsw-taxpayers-to-fund-indemnity-for-47-organisations-against-child-abuse-claims

Leave a Reply